Estate Deductions Subject To 2 Floor

Checklist Of Documents Required For Filing Tax Return Of Salaried Person Download This Checklist From Https Taxdosti Com Filing Taxes Tax Return Informative

Notice Of Late Rent Free Printable Documents Late Rent Notice Rental Property Management Rent

Printable Sales Contract For Buying Subject To Template 2015 Real Estate Contract Real Estate Forms Contract Template

To Know The Tax Benefits Provided To First Time Home Buyers Watch Out Image Below To Grab These Benefits Just Call Out 8852 Finance Loans Loan Investing

Free Offer To Purchase Real Estate Pro Buyer Form Wholesale Real Estate Real Estate Forms Real Estate Contract

Final Rules On Fiduciary Fees Are Issued Accounting Programs Estate Tax Tax Deductions

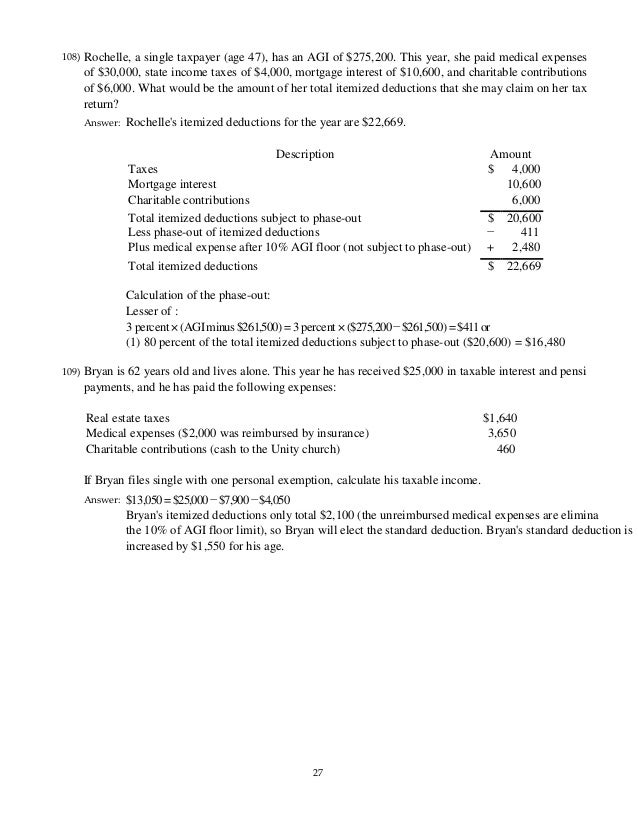

Examples of itemized deductions not subject to the 2 floor include costs related to fiduciary income tax returns and estate tax returns probate court costs and certain appraisal fees.

Estate deductions subject to 2 floor.

Acct 426 Tax I Chapter 10 Flashcards Quizlet

Month To Months Residential Rental Agreement Free Printable Pdf Format Form Rental Agreement Templates Lease Agreement Free Printable Room Rental Agreement

Offer Letter Format In Word In 2020 Letter Format Sample Letter Templates Free Lettering

Subject To Existing Liens Aka Sub 2 Real Estate Contract Download Now Real Estate Contract Real Estate Investing Positive Cash Flow

Available Homes Mcguinn Homes New Homes In Columbia Sc Publisher Clearing House Home Buying Home

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Personal Assistant Agreement Best Of 32 Sample Contract Templates In Microsoft Word Peterainsworth In 2020 Contract Template Contract Templates

Printable Sample Free Printable Rental Agreements Form Lease Agreement Rental Agreement Templates Room Rental Agreement

Home Improvement Contractia Requirements Sample Nyc Template New York In Photos Hd Didierrecl Construction Contract Roofing Contract Residential Construction

Driving The Same Car For Business And Personal Use Photography Business Tips Articles Photography Office Tax Preparation Quotes About Photography

Mending The Piggy Bank Budgeting Spreadsheet Budget Spreadsheet Budgeting Spreadsheet

Tax Time Tax Time Home Business Business Magazine

Buffer A Smarter Way To Share On Social Media Backyard Views Garage Style Backyard

New Irs Regulations Regarding Trust And Estate Costs And Expenses Fiskeco Com Fiskeco Com

Pergola Front Porch In 2020 Pergola House Styles Front Porch

The Cost Per Unit Of Keeping Your Home Warm The Unit Home Com Home Schooling

Million Mansion That Is Still On The Market Photos And Premium High Res Pictures Stone Mansion Mansions Exterior

On Valentine 039 S Every Other Day We Love Lawsuits Infographic In Law Suite Legal Nurse Consultant Infographic

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqcdbqvym69vi4utfsvxea881toz9v0klyqhcahwzdcifur8gfq Usqp Cau

709 S Walnut Street Floor Trim Marysville Hardwood Floors

House Warming Gift Artwork From A Photo In Pen Ink From Giveamasterpiece Com House Portraits Custom House Portrait Photo Art Gallery

50 Cent Battles In Bankruptcy Court To Save His Connecticut Mention Former Home Of Iron Mike Tyson Is Subject In 50 Cent Mike Tyson 50 Cent House Poplar Hill

Open House Welcome Sign No 2 Open House Real Estate Real Estate Signs Open House Signs

Custom Testimonial Prop Home Buying Tips Real Estate Tips Real Estate Signs

Source : pinterest.com